Travel and Eating Out Are What Americans Have Been Missing Most

Survey findings tell us consumers are more eager to resume some pre-COVID activities than others.

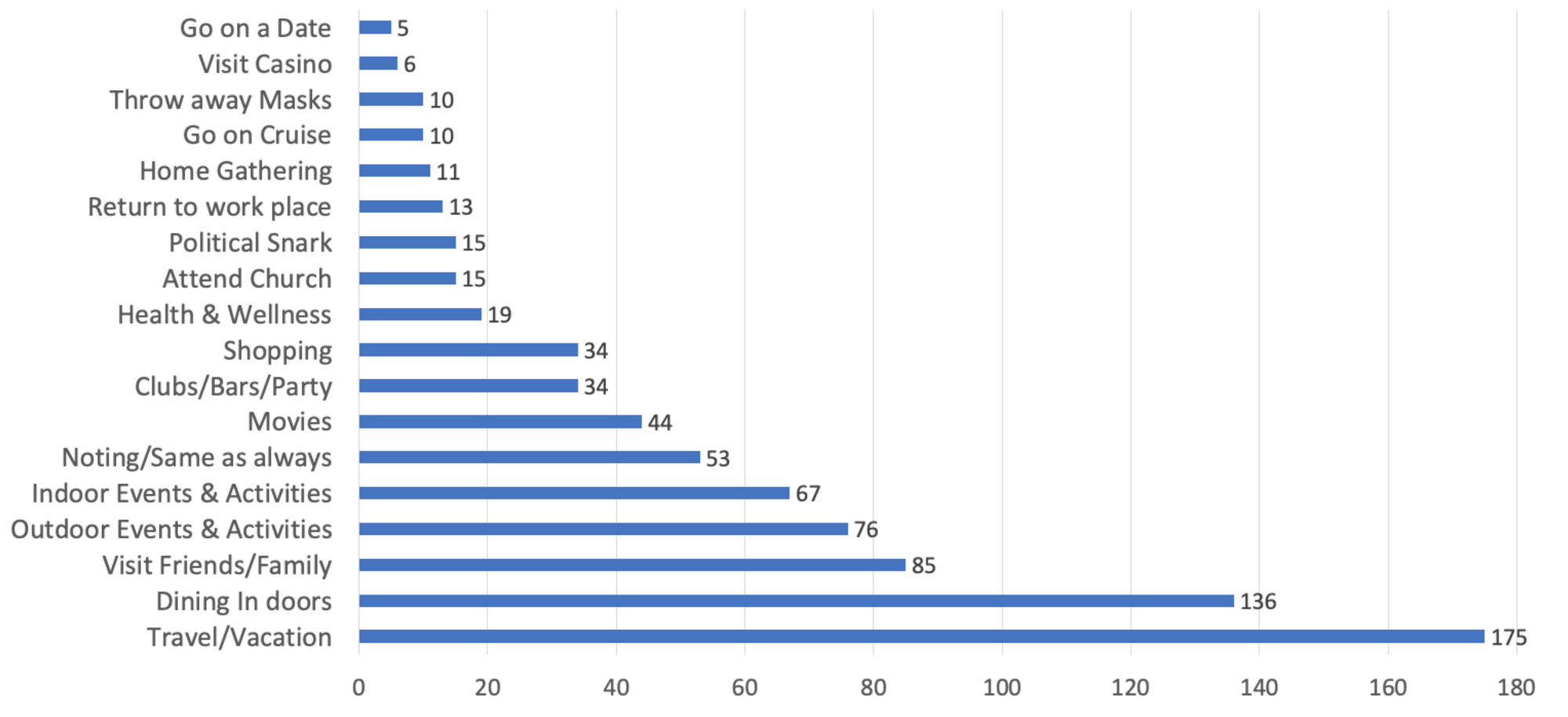

- We surveyed 500 US adults: “When you feel safe and the economy opens up, what are three things you plan on doing?”

- The top three intended activities were travel, indoor dining and visiting friends and family.

- People were much less interested in going to movies, bars, shopping, exercise, haircuts, church and dating.

The latest pandemic-lockdown in the UK ended this week, prompting people to rush out to pubs to celebrate with morning drinking. More significantly, people also went back into retail stores in a forceful display of pent-up demand for in-store shopping.

Americans are also eager to return to “normal life.” And many of them are doing so already, In fact, so much so that it’s creating new COVID hotspots. Yet many people remain cautious about resuming pre-pandemic activities, although confidence is growing about going out again.

Gauging Pent-Up Demand

One of the questions we’ve been writing about and discussing on The Near Memo podcast is how different post-COVID activity will be from pre-pandemic behavior.

To test the pent-up demand thesis, Mike fielded a survey of 500 US adults using Google Consumer Surveys. He asked, “When you feel safe and the economy opens up, what are three things you plan on doing?”

Unlike most surveys this one was entirely open-ended. It didn’t prompt or lead respondents with multiple-choice options. The results reflect the top-of-mind, unaided thinking of consumers (18-65+) from across the US. The sample pretty closely matches the US population distribution.

Travel, Eating Out, Friends & Family

Respondents could provide up to three answers, many provided only one. The top three intended, post-COVID activities were:

- Travel/vacation

- Indoor dining

- Visit friends/family

When the economy opens up what 3 things do you plan on doing?

Travel was arguably the hardest hit of all major industries during 2020. The survey finding suggests it will make a strong comeback in the second half of 2021 and 2022. There are already indications that bookings are picking up quickly. The lack of interest in cruises, however, shows not all travel segments will recover as fast.

Eating out (or in) in restaurants is the number two intended activity. Indoor dining has returned in many places and some restaurants are seeing it pick up rapidly, for better and worse. One could argue that more than any other item on the list, eating out is a stand-in for normalcy in general.

Here are a few representative comments from survey respondents about things they were looking forward to:

- "Traveling with my family, making a list of all the things I want to do while places are open and get a haircut"

- "Having a BBQ, hug my nieces and nephews and visiting a family member"

- "Going out to eat, go to a baseball game, shop in a department store"

- "Seeing aging grandparents."

Surprises: Shopping, Drinking, Salons, Dating

Unsurprisingly, “visit friends and family” is number three on the list – as suggested by some of the remarks above. What’s a bit more surprising is the relatively weak showing by activities we would expect to be ranked higher: movies, bars, shopping, exercise, religious observance and dating. In particular, health and wellness, which includes going to the gym and haircuts, made a generally poor showing. (I've had one haircut in the past 14 months.)

Despite the finding of apparently lackluster interest in going out to movies, the recent US box office success of Godzilla vs. Kong argues people will be going back into theaters, at least selectively. Yet the low priority placed on shopping might mean they will be careful and not immediately rush out to retail stores across the board. Then again, data from Gravy Analytics shows overall monthly retail foot traffic growth in the US of 11.6%.

Regardless, of discrepancies between the survey and third party data, what these findings tell us that consumers aren’t equally focused on resuming all their old activities equally or immediately. Some of them may come roaring back while others, in the absence of discounts or other incentives, will take considerably longer.